Studying Ant’s Cash Cow

A dive into Huabei, the microloan credit card

Author’s Note: This video is quite long, but I never had the time to go into the news breaking about the actual reforms Ant Group need to implement. Bloomberg goes through them, but here’s a summary.

The new rules force Ant to make some of the micro-loans itself and hold them on their books. Previously, Ant only needed to make some 5% of those loans. At the time of the IPO, Ant was holding just 2%, not even reaching those rules. The draft rules are going to raise that threshold to something like 30%.

This essentially will force Ant to be more like a bank. The way banking works, if you make loans that you keep on your books, you need to also hold enough cash to reasonably cover defaults on those loans. This caps the amount of loans you can make and thus limits the segment's profitability.

Furthermore, it looks like the government is going to try to cap the total amount of loans made to an individual to 300,000 RMB ($15,000 USD). Or no more than a third of the borrower's average income in the past 3 years.

It is also just a lot of money to raise. Some analysts estimate that Ant will need to raise some $12 billion in money. That is probably going to need be done by selling stock. This dilutes the holdings of current shareholders.

New rules still in the draft stage will make it hard for the Ant Group platform to operate nationally. Bloomberg says that online microlenders cannot go outside their provincial base without a license. Not quite sure if that one goes through, but if it does then my guess is that it will carve up the country's financial businesses into fiefdoms by province. If you are asking me, that’s a better thing for the economy. It means more competition between competing firms. It means an opportunity for small companies to grow.

Ant Group is one of the biggest private companies in the world. And it was about to go public in a dazzling, record-setting debut. Until it couldn’t. And then suddenly things went very wrong very fast.

There have been a lot of news that the Ant IPO would be delayed for over a year, which goes to say a whole lot about the level of reforms that the government thinks the company needs.

The key regulation has to do with Ant's super-profitable micro-lending platform. The way it is set up right now, it mints money. China is about to chop it down to size.

Introducing Huabei

In its IPO documents, Ant Group organizes its business lines into Digital Payments, Credit, Investment and Insurance. Digital Payments is the Alipay stuff. It processes payments between buyers and sellers kind of like PayPal.

CreditTech is the credit business and the focus of this discussion. In the IPO documents it is described as:

Our CreditTech services address the unmet credit demands of unserved and underserved consumers and small businesses in China. We openly collaborate with our partner financial institutions through our technology platform. We originate loans, which are then independently underwritten by our partner financial institutions. As of June 30, 2020, we worked with approximately 100 partner banks ... We generate technology service fees from our partner financial institutions that are based on the credit balance originated through our platform. Our approach is not to use our own balance sheet or provide guarantees.

This segment also happens to be Ant's flagship money machine. It grew 59% in the first six months of 2020. It now contributes some 40% of Ant’s revenues. It is likely quite profitable.

The key consumer product behind this CreditTech platform is a service called Huabei (花唄, literally translated as "just spend"). There is another one called Jiebei (借唄) which is similar, but I am going to focus on Huabei.

Note: I would probably describe Jiebei as more of a high-end product positioning as compared to Huabei. Kind of like how T-Mall is the higher end position than Taobao.

Huabei is called a micro-loan product, but from the perspective of the consumer, it acts like a credit card. Huabei targets young, internet-savvy users who buy things using Alipay. Users who choose Huabei to make a purchase inside Alipay set it as their default. So yeah, it is a lot like a credit card.

Let's talk the interest fees. Huabei's first month (40 days actually) interest is free. Then after that the interest rate goes up to 0.05% a day. Emphasize, a day. So every day you carry a balance on this thing, it adds another 0.05%. You can pay that back monthly or in installments. If you pay back your loans, then its smart machine learning algorithm decides that you are a creditworthy customer and steadily raises your limit.

Ant also makes money from merchants who pay a processing fee (0.8-1% of the transaction) to be featured within the Huabei system. Presumably, the convenience of offering Huabei means that consumers are more likely to buy from you.

Ant does not make money from the loan or the loan's interest. Like as its prospectus says, Ant does not lend its own money. It is lending the money from its partner banks. There are over a hundred such banks. Ant also makes fees securitizing and selling those loans to investors - kind of like with the sub-prime mortgage thing.

This way, Ant presumably does not take on the credit risk of the loans that it makes. Partnering with the banks also subtly co-opts resistance from the financial industry by cutting them a piece of its business flow.

Just what really is this thing?

If the above sounds a bit familiar to you, then you are not far off. If you phrase it in the way I just did, Huabei acts kind of like Visa or MasterCard. Visa and MasterCard are payment networks that help facilitate online and convenient payments. They do not issue the loans themselves, those are done by the bank issuing the card. Visa and MasterCard provide a network that connects buyers and merchants - and for that convenience they take a 1-2% fee.

If you believe that Huabei is Visa and MasterCard, then it would be an amazing business. Visa Inc is a $450 billion company. The company makes $23 billion a year in revenue and over half of that revenue falls right to the bottom line as net profit. That's fantastically profitable. Furthermore, Visa does not take on the loan default risk from transactions on its network.

But at the same time, there are a lot of things about Huabei that differentiate it from just a simple payments network.

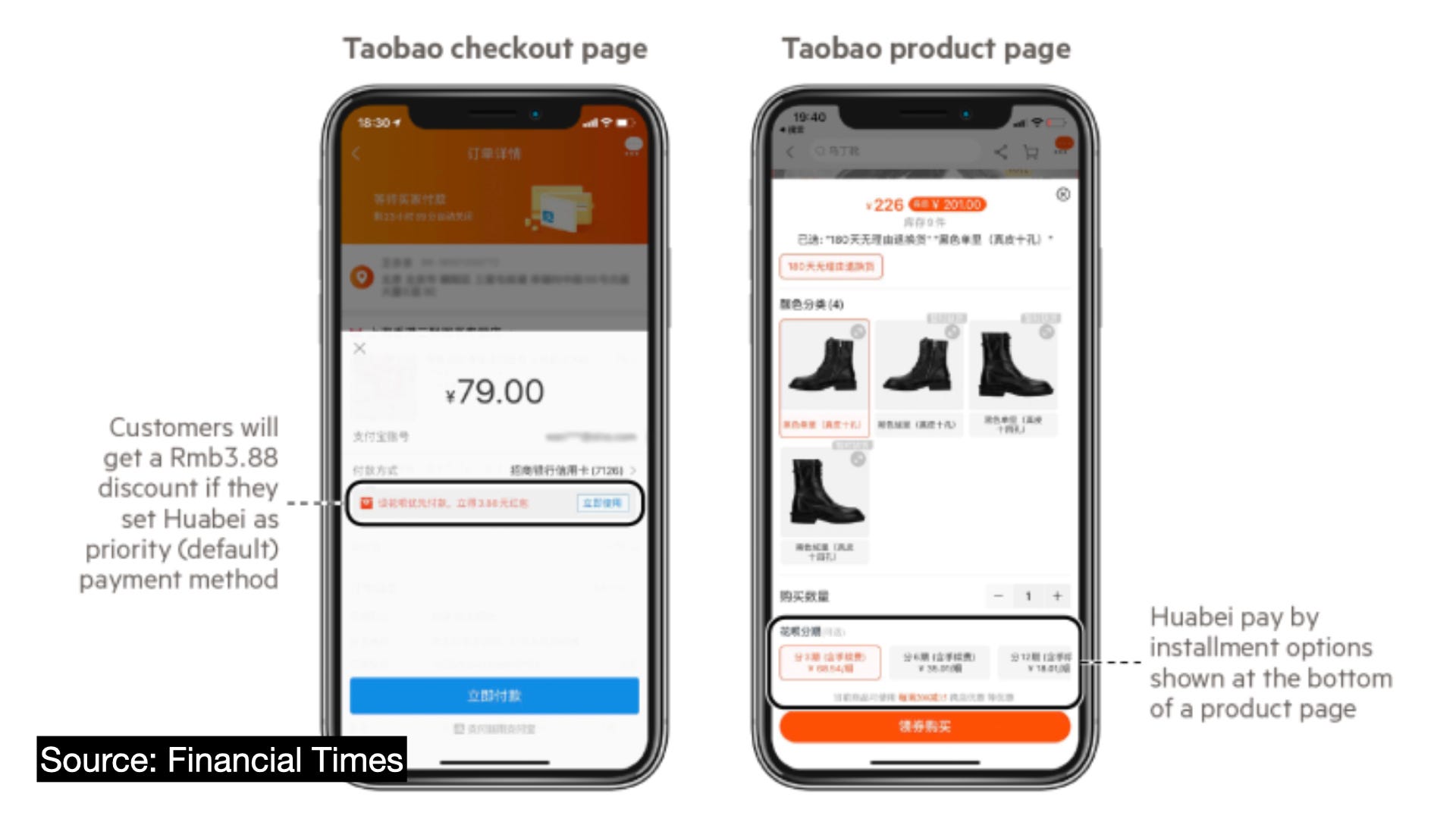

For one thing, Huabei is so closely tied to the Alipay and Alibaba ecosystem. The app pushes the Huabei product very aggressively. They regularly run promotions for it. For example, they will randomly give away 50 cents free to a customer if they make Huabei their default payment system.

Taobao is the dominant e-commerce site in China. Kind of like its Amazon. If you want to make a purchase in Taobao, Huabei is there to help you. Taobao will give you a small discount (small as 50 cents maybe) to use Huabei to check out. Do so, and then Huabei becomes the default rather than the normal digital cash balance on the app.

I don't think Visa has a mobile app that people use on a regular basis for payments. Visa does not issue you a credit card that is also a debit card and then makes the credit card the default every time you swipe at Wal-mart.

And as many people know, defaults are powerful. Once Huabei is the default, it sits on top of all of a customer's purchases. Then you start getting the horror stories about ordinary Chinese people finding themselves locked in a cycle of never-ending credit card debt. Regardless of whether they be Chinese or American, card debt can happen to anyone. Probably worse for Chinese since there are millions of people who had never grown up with something as convenient as a credit card.

In addition, there is something to be said about the credit business's sheer size and the systemic financial risk posed by that size. The IPO documents say that the average outstanding balance as of June 30, 2020 is just $295 or 2,000 RMB. But China is all about scale, and Alipay has some 700 million users. Huabei specifically is used by 400 million people.

Ant by itself is the source of some 10% of all the loans generated by China's financial system. Its loan volume in the first half of 2020 was over 1.7 trillion RMB. Far larger than any one bank, including any of the Chinese Big Four.

(Not to mention that those loans are going to act almost all the same since they have all been approved using the same algorithm. Think the credit rating agencies before the Global Financial Crisis)

When you combine a general public unfamiliar with how debt works with a massive organization heavily incentivized to make as many loans as possible, you got a recipe for financial disaster.

How Ant got here

Ant so aggressively pushes Huabei because Alipay otherwise does not seem to make money. The independent business magazine Caixin recently reported that Ant's payment business - the segment that kicked off Alipay in the first place - does not make money. It used to be the company's cash machine, but then Tencent started WeChat Pay and that kicked off a massive battle between the two tech titans. Huge subsidies and technology product costs were incurred to gain an advantage.

Note: Many of the regulations that apply to Alipay will probably apply to WeChat Pay too by the way. I haven’t even touched on the WeChat Pay thing. I am curious why not more hay is made out of the fact that WeChat Pay launched a payments product and basically eroded away all of Alipay’s payment transfer profits. Stock analysts were so excited about Alipay back in the 2000s, calling it a monopoly. Seems like the Chinese market is too dynamic to call any private company a monopoly.

Then in 2017 the government regulated that bank payments need to be routed through a government clearing system. This basically turned the business into a low-margin grind. The Chinese government apparently did this as part of their clampdown on capital flight.

With their old transactions business pinched off, Alipay apparently decided to build a payment card network like Visa and MasterCard. But a card network is hard to build and China already has UnionPay. UnionPay is no longer a monopoly, but it took Amex, Visa and MasterCard half a decade to get a China license for their network (and the process is still not done yet).

Alipay created their own private credit card network and let it grow to immense size without virtually any oversight. That's what they did wrong. Is it really financial innovation if it's just the same thing over again, but worse?