How TSMC Might Spend $28 Billion

Author’s Note: This is an abridged version of another video. Since it is a bit more tied in to current affairs, I wanted to share a chunk of it with newsletter subscribers first.

If you are interested in seeing the whole version or want to watch some of the other videos waiting to be released (right now I think there are nine), check out the Patreon and its Early Access Tier.

TSMC recently released their Q4 2020 quarterly financial report. The results were quite good.

TSMC has become one of the world's most profitable companies. In 2020, the company generated net income of something in the neighborhood of $17.5 billion (depending on the USD-TWD exchange rate). TSMC generated more 2020 profit than Wal-mart or Tencent and roughly as much as Facebook. Its products make 53% gross margin, which matches Intel's reported 53% gross margin in Q3 2020. Though Intel has a lot of moving parts and that probably brings things down a bit.

But the big surprise was not the profit but TSMC's company guidance for Q1 2021 capital expenditure. Capital expenditure represents expenses spent on expanding overall capacity and upgrading manufacturing technologies. This number is a long term leading indicator of where TSMC believes the market is to be.

In 2020, TSMC spent $17.2 billion in capital expenditures. This is a billion over the $15-16 billion range that they had projected back in 2019. They had raised it midway through the year. The $17 billion was a record for the company.

Analysts had expected the company to announce $20 billion of capital expenditure for 2021. It would roll over the $17 billion from 2020 and add the capital for the Arizona plant. TSMC had earlier announced in November 2020 that they were going to build a small N5 fab in Arizona. The board allocated some $3.5 billion for this.

Well, this $20 billion in retrospect was far too little. For 2021, the company announced that that they will spend something in the range of $25 to 28 billion.

A lot of words have been spilled on the internet, trying to figure out why the jump in capital expenditure. Right now I am just trying to grapple with the sheer size of the number.

$25 billion, the lower end of that number, would represent as much revenue as Mondelez, the Oreos maker and number 117 on the Fortune 500. It would be more than Tesla's 2019 fiscal year revenues ($24.5 billion). $28 billion would be the size of Starbucks ($26.5 billion) or ViacomCBS ($27.8 billion).

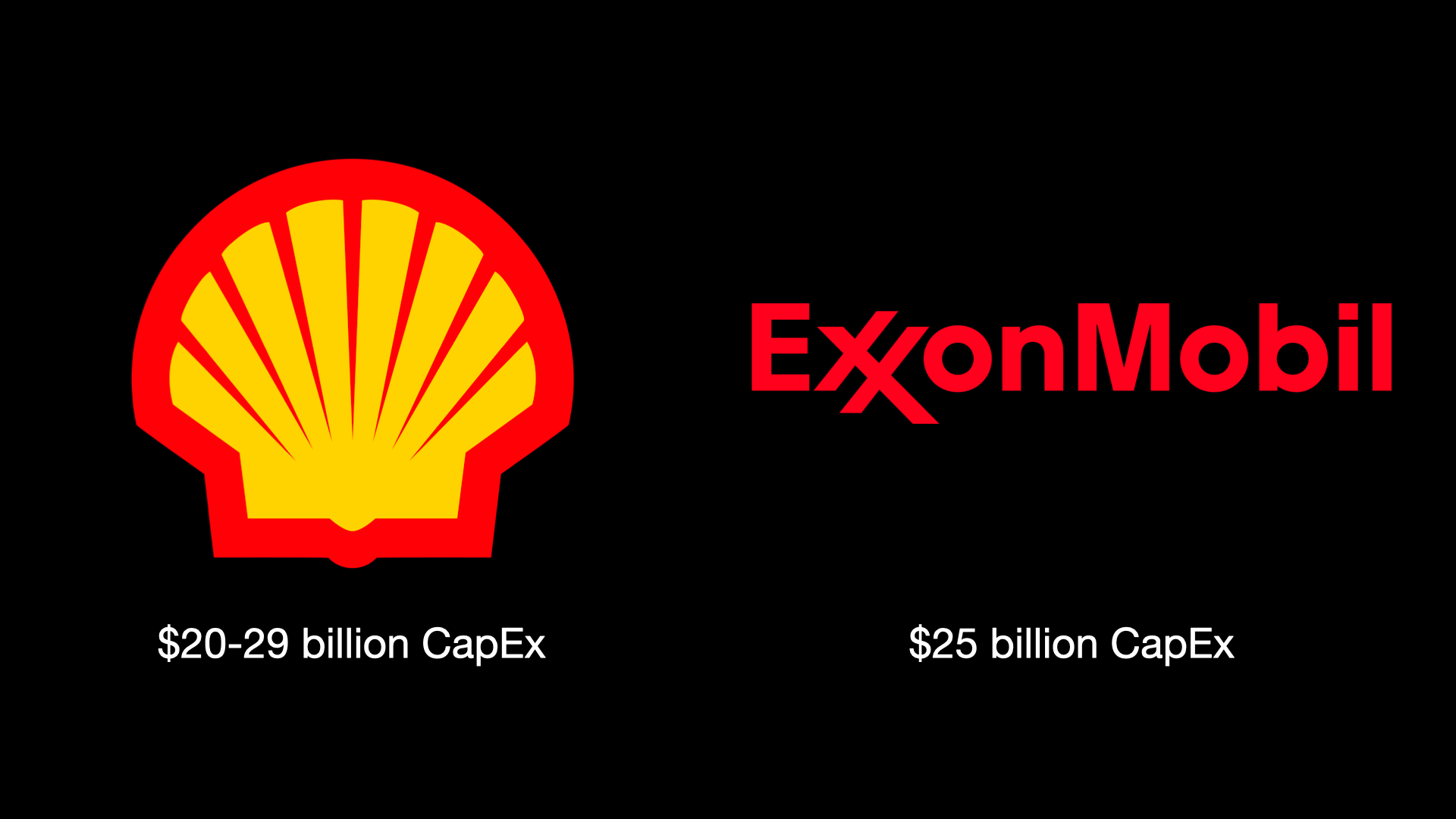

In terms of sheer numbers, TSMC’s budget rivals capital expenditures from tech giants and telecoms. That includes Verizon ($17.9 billion) and Google ($25 billion). Anytime you’re building big data centers and installing new networks, you are spending billions of dollars on building up things and assets. Oil and energy companies like Exxon ($25 billion) and Royal Dutch Shell ($20-29 billion) are also peers.

Amazon has a demonstrably higher budget with $32 billion. But Amazon is also scaling up immensely as it tries to dominate the e-commerce and cloud spaces.

For me, I think you don't spend $25-28 billion just for one reason alone. There must be a multitude of reasons.

Astounding Demand

The first has to do with demand from the unprecedented economic environment. The first wave led to everyone shutting down and the economy crashing hard - but then it came roaring back faster than people thought was possible.

At the same time, the work from home economy came back harder than ever after the summer ended and the pandemic surged. You need chips to fuel all those cloud software services connecting today's companies.

Another source of demand comes from your car. On the earnings call, TSMC mentioned the automotive industry, where revenue surged 27% from the previous year. Your car uses a surprisingly high number of chips to help it operate. The Wall Street Journal recently ran an article noticing that a chip shortage in the automotive industry has caused some factories to wait for supply to replenish.

Automotive, financial stimulus, a new generation of video game consoles, lockdowns from the pandemic's second surge. In addition, we have chip demand stemming from the new crypto surge and the ongoing 5G transition. It's all insanity and craziness.

Competition

The second big reason to really push hard has to do with competition. TSMC is dealing with a challenger unlike few others that it has gone up against. Samsung Foundry, part of Samsung Electronics is making a real push into the market - capturing reliable business as a second supplier.

The Korean giant is estimated to spend some $26 billion in capital expenditures for its own semiconductor business in 2020. There is the caveat that Samsung is also the world's dominant memory maker and it is assumed that a vast majority of that capital is going into reinforcing that business. Not all of that can be leveraged for making logic chips. But that is a lot of money regardless. It needs a response.

But Samsung is really swinging for the fences. For its cutting edge 5 nm process, the company has collected customers like Ambarella (the image sensor maker and supplier to Hikvision) and Qualcomm. They have a big Austin semiconductor foundry and are considering a $10 billion Texas investment, similar to Taiwan's Arizona facility, so to win more American clients.

And then there is the anticipation that Samsung is seeking to implement a brand new semiconductor structure for its next generation 3 nanometer node; something called "Gate All Around". TSMC's N3 will not be using this structure, and for this reason Samsung has been cited as seizing the technology crown upon the release of that 3 nanometer process.

Intel

A lot of financial analysts were watching this. Intel CEO Bob Swan had said that the company would look at the possibility of outsourcing its high end logic chips to a third party foundry like TSMC or Samsung. Such a decision would be announced at the Q4 earnings call in Jan 2021.

There were a lot of smoke signals coming up that Intel would be indeed signing on to such an outsourcing agreement. The stock market ran up TSMC's stock price in anticipation of it happening. Bloomberg ran an article saying that TSMC and Intel had been in talks, with no result.

Then Bob Swan stepped down and new CEO Pat Gelsinger took up the seat. Intel's first CTO, Gelsinger has an engineering background and in the Q4 call emphasized Intel's commitment to its engineering and manufacturing:

“I am confident that the majority of our 2023 products will be manufactured internally ... At the same time, given the breadth of our portfolio, it’s likely that we will expand our use of external foundries for certain technologies and products.”

The stock fell 9%. An interesting response by the market. There is a real argument for semiconductor foundry work to be done on American soil. One can say that the market is ignoring those national security arguments and being short term. But one can also care for those arguments and just instead be saying they don't think Intel should be the company leading that charge.

Putting those questions aside, the Intel and TSMC relationship is going to put itself on hold for a little bit as management reviews the status of their 7 nanometers process (roughly equivalent to TSMC's N5).

Conclusion

I get the sense that TSMC is a company that likes to take big swings at things. Unlike Chartered and SMIC, they have the power of the purse and they leverage it like few other companies can.

A famous investor once said that their entire job is to stand at the batter's box and wait for a fat pitch that they can swing at as hard as they can. Hit one big home run and it does not matter that you missed a bunch of little things. I think TSMC thinks a fat pitch is coming.

Do you feel TSMCs comments about Automotive (and AI) leading the push toward growth, alongside their long-term SSMC JV with NXP, point to any sort of large-scale collaboration upcoming between these two companies as semis in Autos continue to face shortages?

https://www.gigaphoton.com/en/technology/euv-topics/status-of-world-research-in-euv-lithography